contents

Introduction

1 THEORETICAL ASPECTS OF FISCAL POLICY: TAXATION

1.1 Fiscal policy

1.2 Taxation

1.2.1 MAJOR TAXES and DUTIES

2 Features of Residents and Nonresidents taxation

2.1. Features of Resident

2.2

Permanent establishment of a nonresident

2.3 Nonresidents’ income from sources in the Republic of Kazakhstan

2.4 Procedure for the taxation of the income earned by nonresident legal entities doing business without creating a permanent establishment in the Republic of Kazakhstan

2.4.1

Procedure and deadlines for the payment of income tax at the source of payment

2.4.2

Provisions specific to the calculation and payment of income tax on

capital gains from the realization of securities

2.5 Procedure for the taxation of the income earned by nonresident legal entities doing business through a permanent establishment

2.5.1 Procedure for taxation of the net income of a nonresident legal entity from doing business through a permanent establishment

2.5.2 Procedure for taxation of the income of a nonresident legal entity in certain cases

2.6 Procedure for the taxation of the income of income of nonresident individual

2.6.1

Procedure for calculation and payment of the income tax on a nonresident individual whose activities lead to the creation of a permanent establishment

2.6.2

Procedure for the taxation of a nonresident individual’s income in certain cases

2.6.3

Procedure and deadlines for prepayment of the individual income tax

2.6.4

Statement of anticipated individual income tax and individual income tax return

2.7 Special provisions regarding international agreements

2.7.1

Proportional distribution of expenses method

2.7.2

Direct deduction of expenses method

2.7.3 Procedure for payment of the income tax on income earned by nonresidents from activity in the Republic of Kazakhstan not leading to the creation of a permanent establishment

2.7.4

Procedure for the application of an international agreement with respect to taxation of income from providing transportation services in international shipping

2.7.5

Procedure for the application of an international agreement with regard to the taxation of dividends, interest, and royalties

2.7.6

Procedure for the application of an international agreement with regard to the taxation of net income from doing business through a permanent establishment

Реклама

2.7.7

Procedure for the application of an international agreement with regard to the taxation of other income from sources in the Republic of Kazakhstan

2.7.8

General requirements for the filing of a request to apply the provisions of an international agreement

Conclusion

Appendix A

Appendix B

THE LIST of USED SOURCES

Introduction

The taxes are a necessary part economic activity in a society from the moment of occurrence the states. Development and change of the forms of the state system always lead to transformation of tax system. Taxes – is basic sources of incomes of the state in a modern civilized society. Besides this especially financial function, taxes are used for economic influence of the state on public manufacture, its structure, and on condition of scientific and technical progress.Among economic levers, through which the state influences market economy, the important place belongs to the taxes. In conditions of market economy any state widely uses tax policy as the regulator of influence on the negative event in the market. The taxes, as well as all tax system, are the powerful tool of management of economy in terms of the market. The application of the taxes is one of economic methods of management and maintenance of interrelation of nation-wide interests with commercial interests of the businessmen and enterprises, independent from departmental subordination, patterns of ownership and legal form of the enterprise.

With the help of the taxes determined the mutual relation of the businessmen, enterprises of all forms is the properties with the state and local budgets, with banks, and also with higher-level organizations. Through the taxes the foreign trade activities are adjusted, include the attraction of the foreign investments.

The tax system in Kazakhstan is based on the Tax code enacted by the president’s Decree that has the force of Law on Taxes and other obligatory Payments to the Budget The taxes are the basic source of formation of a profitable part of the budget of Republic of Kazakhstan. Not last role in it plays the taxes from the nonresidents. According to the legislation on Kazakhstan foreign citizens - residents in the Republic of Kazakhstan (RK) are subject to individual income taxation on their worldwide income. Foreign citizens - nonresidents are subject to taxation only on income received from Kazakhstan sources. The following types of nonresidents’ income, among others, should be considered as received from sources in Kazakhstan:

Реклама

· Income received from operations in the RK under individual labor agreements (contracts) or under other agreements of a civil-legal nature;

· Directors fees and /or other payments received by members of aboard of a resident legal entity, regardless of the place of the actual performance of their functions;

· Fringe benefits received in connection with their assignment to Kazakhstan its rates;

Payment and other conditions are regulated by the chapters 7, 10, 12, 15, 18 and other of Law on Taxes and other obligatory Payments to the Budget. Taxation of foreign citizens in the RK is also regulated by Conventions (agreements) on the avoidance of double taxation. In case there is a Tax Convention signed between Kazakhstan and the other foreign state, which may be applicable to a foreign employee, then the status of residency is determined in compliance with this Convention. The Tax Conventions do not regulate procedure of filing and regularity of tax payments. However, based on the status of residency of a foreign employee determined by the Tax Conventions specific reporting and taxation requirements stipulated by the Kazakhstan tax legislation should be fulfilled with respect to residents or nonresidents in the RK. In case the foreign employee is a resident of the other foreign state, then he/she should be considered as a nonresident for taxation purposes in Kazakhstan. In this case the foreign employee should file a Certificate on the Estimated Personal In-come Tax and pay personal income tax through the monthly transfer of advance payments. In case a foreign employee is considered as a resident of Kazakhstan, then the statutory rules do not contemplate filing of the Certificate on the Estimated Personal Income Tax and contemplate in-come tax payment once a year at the time of filing the income tax return from an individual for a year.

1.

THEORETICAL ASPECTS OF FISCAL POLICY: TAXATION

1.1 Fiscal policy

Fiscal (lat. fiscalis - state) policy (politics) - is the aggregate of financial measures of the state on regulation of the governmental incomes and expenditures. It changes significant depending on put strategic tasks, as for example, anticrisis regulation, maintenance high employment, struggle with inflation.

The modern fiscal policy defines basic directions of use of financial resources of the state, means of financing and main sources of updating of treasury. Depending on concrete - historical conditions in different countries such policy (politics) has its own features. At the same time in Developed Countries is used set of common measures. It includes straight and indirect financial methods of regulation of economy.

To straight ways concern the means of budget regulation. By the means of the state budget are financed:

1) expense on expanding of reproduction;

2) unproductive expenditures of the state;

3) development of an infrastructure, scientific researches and etc.:

4) realization of structural policy (politics);

5) the support of military producers complex etc.

With help of indirect methods state influences on financial opportunity of the manufacturers of the goods and services and on the demand sizes of customer. The important role here plays the System Taxation. Changing the rates of the taxes on various kinds of the incomes, giving tax privileges, reducing free minimum of the incomes etc., state aspires to achieve probably steadier rates of economic Growth and to avoid sharp rises and falls of manufacture.

To number of the important indirect methods assisting accumulation of the capital, is the policy (politics) of the accelerated amortization. On the essence, the state exempts the businessmen from payment taxes with part of the profit, is artificial redistribute it in amortization fund. So, in Germany in the beginning 70 years on a number of industries on amortization it was authorized to write off till 20-30 of % of cost of a fixed capital in one year. In Great Britain in first year of introduction in using of the new equipment it was possible to deduct in fund of amortization 50 % of cost new instruments of manufacture.

However in these cases the amortization is written off in the sizes, that significant exceeding the valid deterioration basic capital, in consequences the raise of price on made with the help of this equipment production. If accelerated amortization expands financial opportunities of the businessmen, simultaneously it deteriorates the condition of realization of production and reduces purchasing power of population.

Depending on character of use direct and indirect financial methods distinguish two kinds of fiscal policy of the state:

a) Discretion

b) Non-discretion.

a)

Discretion (lat. discrecio - working on itself discretion) the policy (politics) means the following. The state consciously regulates its expenditure and taxation with the purposes of improvements economic of situation of the country. At the same time government takes into account the following checked up on practice functional dependences between financial variable.

The first dependence: the growth of the state expenditures increases cumulative demand (consumption and investments). Thereof increase output and employment of the population. Is important to take into account, that state expenditures influence on cumulative demand the same as to investments (work as the animator of investment which has developed J. Keynes). The animator state expenditures MG shows, how much grows total national product D GNP in result of increase of these expenditures DG:

D GNP =DG ' MG

It is natural, that at reduction of state expenses G reduces the volume of GNP.

Other functional dependence shows, that increase the sums of the taxes are reduced the personal available income of household. In this case are reduced demand and volume of production and employment of a labor. And on the contrary: decrease (reduction) of the taxes conducts to increase of the consumer expenditures, production and employment.

The change of the taxation gives multiply effect. However the multiplier of the taxes is less than the multiplier of the investments and state expenditures. Actually increase in unit of a gain of the investments (and state expenditures) is directly influenced on increase in the volume of the GNP. At reduction of taxes, grows available income, however part it goes on the consumption, and stayed share is spent for the savings.

Mentioned functional dependences are used in discretion policy (politics) of the state for influence on business cycle. Certainly, this policy (politics) differs on different phases of a cycle.

For example, at crisis the policy (politics) of economic growth will be carried out.

In interests of growth GNP the state expenditures are increased, the taxes are reduced, and the growth of the expenditures is combined with reduction the taxes so that multiply effect on state expenses was more than multiply effect of the taxes. A result is reduction of recession of manufacture.

When there is an inflationary growth of manufacture (rise, induced by surplus of demand), the government will carry out policy (politics) that hold back business activity - reduces the state expenditures, increases the taxes. These measures are combined so that multiply effect of reduction of the expenditures was more, than multiplier of growth of the taxes. In result the cumulative demand is reduced and volume GNP accordingly decreases.

b)

The second kind of fiscal policy - non-discretion, or policy of the automatic (built - in) stabilizers. The automatic stabilizer - economic mechanism, which without assistance of the state eliminates an adverse situation on different phases business cycle. Basic built - in stabilizers are tax receipt and social payments that are carried out by the state.

On a phase of rise, naturally, the incomes of firms and population grow. But at the progressive taxation the sums of the taxes increased even faster. In this period the unemployment is reduced, well being of needy families is improved. Hence, decrease the payments of the unemployment benefits and others social expenditures of the state. In a result the cumulative demand is reduced, and it constrains economic growth.]

The tendency of transfer payment spending to rise during recessions and fall during expansions results from the bases on which people qualify to receive these payments. People qualify to receive welfare programs only if their income falls below a certain level. They qualify for unemployment compensation by losing their jobs. When the economy expands, incomes and employment rise, and fewer people qualify for welfare or unemployment benefits. Spending for those programs therefore tends to fall. When economic activity falls, incomes fall. people lose jobs, and more people qualify for aid, so spending for these programs rises.

Taxes affect the relationship between real GDP and personal disposable income they therefore affect consumption expenditures. They also influence investment decisions. Taxes imposed on firms affect the profitability of investment decisions and therefore affect the levels of investment firms will choose. Payroll taxes imposed on firms affect the costs of hiring workers; they therefore have -impact on employment and on the real wages earned by workers.

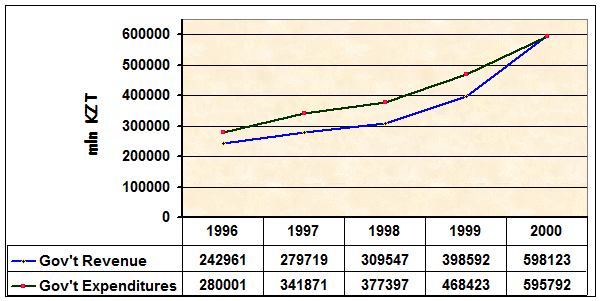

Exhibit below compares government revenues to government expenditures since I996. We see that government spending in Kazakhstan has systematically exceeded revenues, revealing an underlying fiscal deficit between 4 percent and almost 9 percent of GDP, entailing substantial public sector borrowing requirements. Until 1994, fiscal deficit had essentially financed through monetary expansion by the Central bank, with a highly detrimental effect on the rate of inflation during the period. Since then, the National Bank of Kazakhstan has adopted a more independent monetary policy, and fiscal deficits have basically financed either by the proceeds from privatization of state assets or by borrowing foreign loans.

Sources:

Statistics Agency of RK, 2001

On a phase of crisis tax receipts automatically fall and reduced the sum of withdrawals from the incomes of firms and households. Simultaneously grow payments of social character, including unemployment benefit.

At result the purchasing power of the population is increased, that helps to overcoming recession of economy.

From mentioned above it is visible, how large place occupies taxation in financial regulation of macroeconomic. So we can conclude that the main direction of fiscal policy of the state is improving the legislations and practice collection of tax.

Let's take example for the most important version of the taxes – the income tax, which is established on the incomes of physical persons and on profit of firms. How the size of this tax is defined (determined)?

First is counted the total income - sum of all incomes that are getting by the physical and legal entities from different sources. From the total income by the legislation it is usual it is authorized deduct: 1) industrial, transport, the travelers and advertising expenditures; 2) various tax privileges (free minimum of the incomes; for example, in USA in 1990 this minimum was 2050 dollars; the sums of the donations, privilege for the pensioners, disable people etc.). Thus, taxed income is a difference between the total income and the specified deductions.

It is important to establish optimum tax rate (size of the tax on unit of taxation). The following rates of the tax differ:

· hard, which are established on unit of object independently on its cost (for example, motor vehicle);

· proportional, i.e. uniform percent(interest) of payment of the taxes independently on the sizes of the incomes;

· progressive, growing with increase of the incomes.

The practice shows, that at the extremely high rates of taxes discourages to work and to the innovation. Sharp increase in 60-70-е years in western countries of tax burden has resulted the negative consequences. It has caused " Tax revolts ", wide evasion from the taxes, promoted outflow of the capitals and flight of the addressees of the high personal incomes in the countries with one lower level of the taxation.

As it is known, in 70’s neo-conservators have put forward the theory of Supply. Its authors have established, that growth of the taxation renders adverse influence on dynamics of manufacture and incomes. Increase of the taxes at the expense of increase of their rates on certain stage does not compensate reduction of receipts in the state budget because of fast narrowing taxed incomes, and then it can be accompanied also by reduction of total sums of the budget incomes. In a result the high taxes render constraining influence on the offer of the capital, work and savings.

Basic task of economic policy representatives of the theory of Supply consider determining the optimum rates of taxation and both tax privileges and payments. Decrease (reduction) of the taxes is considered as a means capable to ensure Long-term economic growth and struggle with inflation. It will strengthen aspiration to receive huge incomes, will render the stimulating influence will increase by growth of production.

1.2 Taxation

As required by the Constitution of Kazakhstan, within the tax system of Kazakhstan, any taxes, levies, and other obligatory payments may be established only by the laws enacted by the Parliament of the Republic of Kazakhstan. Parliament may not delegate its constitutional powers to establish the tax system, taxes or levies, and sanctions for tax violations to the government or any other authority. Under the Constitution, laws in general and tax laws in particular enter into effect after the President signs them.

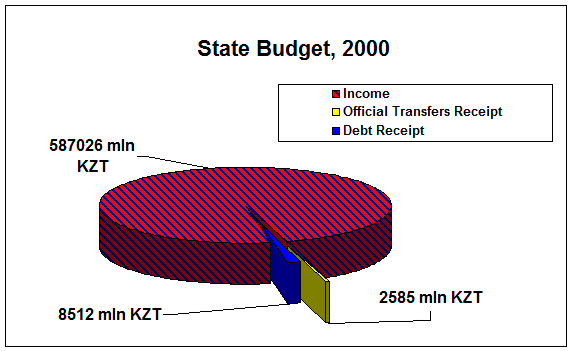

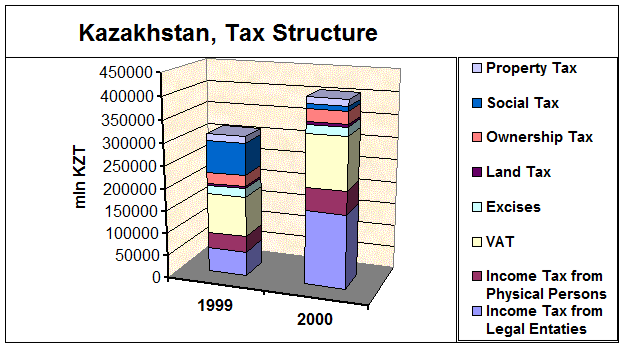

Tax legislation of the Republic of Kazakhstan consists of the Tax Code and Normative Legal Acts, and is regulated by International Agreements. Tax legislation is based on the principles of the mandatory nature of payment of taxes and other mandatory payments to revenue, certainty and equity of taxation, unity of the tax system and publicity of tax legislation. The Tax Code of the Republic of Kazakhstan establishes Kazakhstan taxes, levies, and general tax principles. A tax takes largest share of budget revenues (Appendix A).

Companies formed in Kazakhstan under Kazakhstan law are taxed on world-wide income. Income earned by a foreign company or person through a permanent establishment in Kazakhstan is taxed in Kazakhstan. Branches of foreign entities are taxed on Kazakhstan source income (where services are performed, not where paid for). Income from a Kazakhstan source to a non-resident and not related to a permanent establishment, is taxed at the source of the payment, and further, on the total income without deductions, excluding labor that is taxed as personal income.

Double Tax Treaties

In December 1996, a treaty on the Avoidance of Double Taxation between the United States and Kazakhstan came into force. A number of treaties on the avoidance of double taxation were ratified in 1998. This includes agreements with the following countries: the Czech Republic (November 1998), France (November 1998), Sweden (July 1998), Bulgaria (July 1998), Turkmenistan (July 1998), Georgia (July 1998), Republic of Korea (July 1998), Germany (November 1998), and Belgium (November 1998).

Kazakhstan has double tax treaties with more than 20 countries, which generally follow the OECD Model Income Tax Convention.

| Withholding Tax Rates for Treaty Countries |

| Dividends |

Major Rate

(%) |

Legislative Rate

(%) |

Major Holding

(%) |

Interest

(%)

|

Royalties

(%) |

| Azerbaijan |

10 |

15 |

- |

10 |

10 |

| Belarus |

15 |

15 |

- |

10 |

15 |

| Bulgaria |

10 |

15 |

- |

10 |

10 |

| Canada |

5 |

15 |

10 |

10 |

10 |

| Czech Republic |

10 |

15 |

- |

10 |

10 |

| Germany |

5 |

15 |

25 |

10 |

10 |

| Hungary |

5 |

15 |

25 |

10 |

10 |

| India |

10 |

15 |

- |

10 |

10 |

| Iran |

5 |

15 |

20 |

10 |

10 |

| Italy |

5 |

15 |

10 |

10 |

10 |

| Kyrgyzstan |

10 |

15 |

10 |

10 |

| Lithuania |

5 |

15 |

25 |

10 |

10 |

| Mongolia |

10 |

15 |

- |

10 |

10 |

| Netherlands |

5 |

15 |

10 |

10 |

10 |

| Pakistan |

12.5 |

15 |

10 |

12.5 |

15 |

| Poland |

10 |

15 |

20 |

10 |

10 |

| Russia |

10 |

15 |

- |

10 |

10 |

| South Korea |

10 |

15 |

10 |

10 |

10 |

| Sweden |

5 |

15 |

10 |

10 |

10 |

| Turkey |

10 |

15 |

- |

10 |

10 |

| Ukraine |

5 |

15 |

25 |

10 |

10 |

| United Kingdom |

5 |

15 |

10 |

10 |

10 |

| United States |

5 |

15 |

10 |

10 |

10 |

| Uzbekistan |

10 |

15 |

- |

10 |

10 |

| * Belgium |

5 |

15 |

10 |

10 |

10 |

| Georgia |

15 |

15 |

- |

10 |

10 |

| Iran |

5 |

15 |

20 |

10 |

10 |

| Mongolia |

- |

- |

- |

- |

- |

| Rumania |

10 |

10 |

- |

10 |

10 |

| Turkmenistan |

10 |

15 |

- |

10 |

10 |

| France |

5 |

15 |

10 |

10 |

10 |

| Czech Republic |

10 |

15 |

- |

10 |

10 |

| South Korea |

5 |

15 |

10 |

10 |

10 |

a. Source: Guide on Taxation and Investment in Kazakhstan in 2002, Deloitte & Touche

Notes:

*double taxation treaties with 9 countries listed below are ratified only by Kazakhstan.

|

Tax payment is based on the calendar year, with annual declarations due by end March of the following year (and tax payment within ten days of declaration). Annual financial statements are due April 30 following the reporting year.

Kazakhstan Tax Code, enacted in April 1995, currently apple an international taxation model based on principles of equity, economic neutrality and simplicity. The Parliament approved amendments to the Tax Code by a law dated July 16, 1999; the law was published and became effective August 3, 1999. Following amendments were made in 01 July 2001 and the New Tax Code has become effective January 1, 2002. The Ministry of State Revenues issued tax instructions clarifying the determination and payment of taxes. Resident persons and local enterprises pay taxes on worldwide income; foreign enterprises and non-residents pay taxes only on income from local sources. One is a resident and tax-liable for both direct and indirect income in Kazakhstan if he/she has been physically present in Kazakhstan for 183 days in any consecutive 12-month period.

The penalty for violation of foreign currency regulations constitutes 20 percent of the transaction amount. There are no limitations on the penalty amount to be charged.

All tax laws must be contained in the Tax Code, which covers taxation at all levels of government: central, oblast and local.

1.2.1. MAJOR TAXES and DUTIES

Enterprise Profits Tax is levied on legal entities at the rate of 30%, but 20% in SEZs, and 10% on direct use of land as a sole production asset. All Kazakhstan and foreign legal entities doing business through a permanent establishment must register with the tax authorities regardless of whether they will pay taxes in Kazakhstan or not. Enterprise-related provisions in the Tax Code include: withholding on dividends and interest (15%); taxes on royalties, rentals and service fees; excise and local taxes, and land (10%), property and vehicle taxes; business registration fees, and fees to engage in selected activities. Branches of foreign enterprises operating in Kazakhstan pay a "branch profits tax" applied to their after-tax income. Most business expenses are deductible, including wages, but there are limits on deductibility of reserves for bad debts (actual losses deductible), and research and development. Depreciation is based on pooled asset accounts. Losses can be carried forward for three years.

Individual Income Tax

: Individuals resident in Kazakhstan are subject to personal income taxation on their worldwide income. Nonresident individuals are subject to taxation only on income from Kazakhstan sources. Marginal rates after a small basic deduction, range from 5% to 30% with top rates applied to incomes over $33,700 per year. Most tax is withheld at the source of payment. The tax applies to non-residents' income that is sourced in Kazakhstan only, and to residents' income worldwide, including interest, dividends, capital gains and other income. Taxable income from a Kazakhstan source includes income received under a contract for work or from provision of services, when performed in Kazakhstan, regardless of where it is actually paid. Foreigners must register with local tax authorities and receive a Tax Registration Number within ten days of beginning work under contract in Kazakhstan, or when they become otherwise tax liable as a resident, or receive Kazakhstan sourced income at 500 times a monthly computed basis (about $4,500/year). Foreigners paid abroad must make quarterly estimated payments of income tax and a yearly income tax declaration (due March 31st following the tax year). Foreigners paid locally will have their individual income tax withheld at the source of payment and sent to the Budget by the employers.

Value Added Tax (VAT)

applicable to all goods, work and services, including imports to Kazakhstan. The VAT on imports is usually 16%, and applies to services and goods. Credit for VAT paid on inputs, including Capital investment, is offset against tax on sales. No VAT is paid on exports except to other CIS countries, where by agreement, exports are fully taxed and imports are not taxed (origin principle).

The article provides that sales of textile, sewing, leather processing, and shoe industry products will be zero-rated (0 percent VAT on sales) for residents of Kazakhstan for sales within Kazakhstan. This change represents an important stimulus for the domestic light industry development.

Natural Resources Taxes

include: bonuses paid for the right to resource exploration, royalties paid for the privilege of exploitation and excess profits taxes paid when profits exceed amounts anticipated in setting royalties. Tax rates are set by the Cabinet of Ministers and differ among resources, and are unique to each location and taxpayer. Prohibited: special benefits including lock-in of profits tax rates at conclusion of a Production Sharing Agreement (contract).

Securities Transaction Tax

on new issues of non-government securities, including stocks and bonds: 0.5% of nominal value. Proceeds from secondary transactions are taxed at 0.3%, and 0.1% for government securities. Issuer is liable for tax on initial issues; buyer is liable for tax on secondary transactions.

Unified Land Tax

is levied on peasants and farmers who use private or leased land in their business. The payers of the unified land tax are exempt from corporate income tax, VAT on sales, land tax, transport tax, and property tax. The rate of the unified land tax is set at 0.1 percent of the appraised land value (determined by the Land Committee).

Other Taxes

: A fee for the use of the words "National," "Kazakhstan," "Republic," and their derivatives has been included into the list of taxes in the Tax Code, Business assets are taxed at 0.5% yearly, and individual-owned real estate is taxed at 0.1%.Vehicles are taxed annually depending on vehicle type and engine size.

Double Taxation

. A foreigner won't be taxed in Kazakhstan if:

- he/she is present in the country for less than 183 days in a year and

- his/her income is paid by a non-resident of Kazakhstan and

- his/her income is not taken as a deduction in computing corporate income tax by a permanent establishment in Kazakhstan.

In not distinct cases, where the person is liable to taxation by law in his/her own country and in Kazakhstan, he/she is deemed to reside where he/he has a permanent home, or if he/she has a permanent home in both places, where his/her personal and economic relationships are centered, or in case this cannot be determined, where he/she currently lives and works ("habitual abode"). An individual may offset income tax paid in Kazakhstan against tax owing in his/her home country.

Additional Payments applicable to businesses

Pension Contributions: Employers must pay two categories of pension payment:

15% of payroll paid by companies monthly to the State Center for Pension Payments to be spent on existing pensioners and on state pensions for current employees; ?

10% of employees' gross salaries, not affecting the net pay, transferred for each employee to an accumulation pension fund of that employee's choice.

Excise

:Excise duty is imposed on taxable items produced in, or imported into, Kazakhstan as well as on certain types of activities. Excise duty is imposed on alcohol and tobacco products, motor fuels, diesel, motor vehicles, salmon and sturgeon roe, firearms, crude oil and jewelry. Excise duty is also imposed on gambling businesses and lotteries.

Taxable Products

Excise duty is imposed on alcohol articles covered by Harmonized System numbers 2204 (wine from fresh grapes), 2205 (vermouth and other wines from fresh grapes flavored with plants or aromatic substances), 2206 (other fermented beverages), 2207 and 2208 (ethyl alcohol, spirits, liqueurs and other alcoholic beverages). Excise duty for alcohol products is levied at various rates in KZT per liter.

Excise duty is imposed on tobacco articles covered by Harmonized System numbers 2402 (cigars, cheroots and cigarettes), 2403 (other manufactured tobacco and tobacco substitutes, tobacco extracts and essences). Excise duty for tobacco products is levied at various rates in Euros per 1000 items.

Excise duty is imposed on certain motor fuels covered by Harmonized System number 2710 (diesel, gasoline and jet engine fuels). Excise duty for motor fuels is levied at various rates in EURO per 1000 kg.

Excise duty is imposed on motor vehicles covered by Harmonized System numbers 8703 (motor cars and other vehicles designed for the transportation of persons). Excise duty for motor vehicles is levied at various rates normally in EURO per vehicle’s engine bulk or customs value.

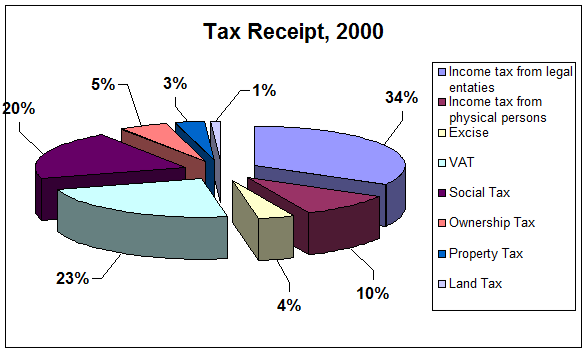

Such taxes as corporate income tax, value added tax, personal income tax, and excise taxes account for the largest portion of budget revenues (Appendix B).

2. Features of Residents and Nonresidents taxation

2.1 Features of Resident

Residents of the Republic of Kazakhstan are individuals who reside permanently in the Republic of Kazakhstan, or whose center of vital interests is located in the Republic of Kazakhstan. An individual shall be considered to reside permanently in the Republic of Kazakhstan for the current tax period if he spends at least 183 calendar days in any consecutive 12-month period ending in the current tax period in the Republic of Kazakhstan. An individual shall also be considered to reside permanently in the Republic of Kazakhstan for the current tax period if the number of days spent in the Republic of Kazakhstan in the current tax period and the preceding two tax periods, determined by applying the following coefficients to each tax period, is equal to at least 183 calendar days:

1 – the number of days spent in the current tax period;

1/3 – the number of days spent in the tax period immediately preceding the current tax period;

1/6 – the number of days spent in the tax period before the one immediately preceding the current tax period.

If an individual has lived in the Republic of Kazakhstan in the current tax period for fewer than 30 calendar days, said individual shall not be considered to reside permanently in the Republic of Kazakhstan. In addition,

an individual shall be considered a nonresident for the period following the last day spent in the Republic of Kazakhstan, unless said person becomes a resident in the year following the year in which the person’s stay in the Republic of Kazakhstan ended.

An individual’s center of vital interests shall be considered to be located in the Republic of Kazakhstan if the following conditions are met simultaneously:

1) an individual is a citizen of the Republic of Kazakhstan or has a permit to reside in the Republic of Kazakhstan (residency permit);

2) an individual’s family and/or close relatives reside in the Republic of Kazakhstan;

3) real property owned by an individual and/or members of his family or held by them on some other basis is located in the Republic of Kazakhstan, and the individual has access to it at any time for use as a residence for himself and/or members of his family.

Individuals who fall into the following categories and who are citizens of the Republic of Kazakhstan or who have filed an application for citizenship of the Republic of Kazakhstan or for a permit to reside permanently in the Republic of Kazakhstan without becoming a citizen of the Republic of Kazakhstan, shall be considered resident individuals, regardless of the time spent in the Republic of Kazakhstan and any other criteria provided below:

persons sent abroad on official business by government agencies, including employees of diplomatic and consular institutions and international organizations, as well as family members of said individuals;

crew members of means of transport belonging to legal entities or citizens of the Republic of Kazakhstan, which make regular international trips;

military and civilian personnel at military bases and those serving in military units, groups, contingents, or formations deployed outside the Republic of Kazakhstan;

persons working at facilities located outside the Republic of Kazakhstan which are owned by the Republic of Kazakhstan or constituent territories of the Republic of Kazakhstan (including on the basis of concession contracts);

students and persons undergoing on-the-job and practical training outside the Republic of Kazakhstan for educational purposes or to gain practical experience, for the entire period of instruction or practical training;

teachers and scientific personnel located outside the Republic of Kazakhstan for the purpose of teaching, consulting, or performing scientific work, for the entire period they are teaching or performing said work.

Also legal entities established in accordance with the legislation of the Republic of Kazakhstan, and/or other legal entities whose effective headquarters (or actual administrative offices) are located in the Republic of Kazakhstan, shall also be considered residents of the Republic of Kazakhstan. Effective headquarters (or actual administrative offices) shall be understood to mean the place where the principal management takes place and where strategic commercial decisions are made which are necessary for the performance of a legal entity’s entrepreneurial activity.

2.2 Permanent establishment of a nonresident

A permanent establishment of a nonresident

in the Republic of Kazakhstan shall be defined as a place of business through which the nonresident performs all or part of its entrepreneurial activity, including activity performed through an authorized person, and specifically:

1) any place of doing business related to the production, processing, assembly, packaging, delivery, or realization of goods, regardless of the duration of the activity;

2) any management office, branch, division, representative office, bureau, office, agency, factory, workshop, production shop, laboratory, store, or warehouse of a nonresident, regardless of the duration of the activity;

3) any place of doing business related to the extraction of natural resources, including the extraction of hydrocarbons: an underground mine, a quarry, an oil and/or gas well, an open-pit mine, land-based or offshore derricks and/or wells, regardless of the duration of the activity;

4) any place of doing business (including monitoring or supervisory activity) related to a pipeline, gas line, the exploration and/or development of natural resources, the installation, set-up, assembly, start-up, adjustment, and/or servicing of equipment, regardless of the duration of the activity;

5) any other place of doing business related to the operation of slot machines (including accessories), computer networks and communications channels, amusement parks, the transportation or other infrastructure, regardless of the duration of the activity.

A construction site, an installation or assembly project, and the performance of planning work shall constitute a permanent establishment regardless of the duration of the work. In this context a construction site (project) shall be understood to mean specifically the place where work is performed to erect and/or renovate real property, including the construction of buildings and structures and/or the performance of installation work, the construction and/or rebuilding of bridges, roads, and canals, the laying of pipelines, the installation of power engineering, industrial, and other equipment, and/or the performance of other similar work. A construction site (project) shall cease to exist as of the day following the day on which the operating certificate for the project (or the acceptance certificate for the work performed) is signed and the construction has been paid for in full.

A nonresident shall also create a permanent establishment in the Republic of Kazakhstan if the nonresident:

1) collects insurance premiums and/or provides insurance or reinsurance coverage for risks in the Republic of Kazakhstan through an authorized agent;

2) provides services on the territory of the Republic of Kazakhstan continuously for more than 90 calendar days in any consecutive 12-month period ending in the given tax period, through employees or personnel hired for these purposes;

3) is a participant in a simple partnership (joint operating agreement) created in accordance with the legislation of the Republic of Kazakhstan and operating on the territory of the Republic of Kazakhstan;

4) holds exhibitions in the Republic of Kazakhstan for a fee and/or at which goods are sold;

5) on the basis of a contractual relationship grants a resident or nonresident the right to represent its interests in the Republic of Kazakhstan, or to act or conclude contracts (agreements, accords) on its behalf.

A nonresident engaged in entrepreneurial activity in the Republic of Kazakhstan through an independent intermediary (a broker and/or other independent agent acting on the basis of an agency, commission, or consignment agreement or another similar type of agreement), who is not authorized to sign contracts on behalf of the nonresident, shall not be considered to be creating a permanent establishment. An independent intermediary shall be understood to mean a person operating within the context of his usual (principal) business, who is both legally and economically independent of the nonresident.

2.3 Nonresidents’ income from sources in the Republic of Kazakhstan

The following types of income shall be considered nonresidents’ income from sources in the Republic of Kazakhstan:

1) income from the realization of goods, the performance of work, or the delivery of services in the Republic of Kazakhstan;

2) income earned from management, financial (with the exception of services involving the insurance and/or reinsurance of risks), consulting, auditing, marketing, legal (with the exception of attorney’s services), agency, and information services provided to residents or nonresidents doing business in the Republic of Kazakhstan through a permanent establishment, and related to said permanent establishment, regardless of where the services are actually provided;

3) capital gains resulting from:

the realization of property located on the territory of the Republic of Kazakhstan;

the realization of securities issued by residents, as well as a share interest in a resident legal entity or in property located in the Republic of Kazakhstan;

4) income from concession of the right of claim on a debt to residents or nonresidents in connection with doing business in the Republic of Kazakhstan through a permanent establishment;

5) charges (fines, penalties) for failure to fulfill or improper fulfillment of obligations by residents and nonresidents, which have arisen in the course of operations by said nonresidents in the Republic of Kazakhstan, including obligations under contracts (agreements, accords) for the performance of work (delivery of services) and/or under foreign trade contracts for the delivery of goods;

6) income in the form of dividends received from a resident legal entity, and income from a share interest in such a legal entity;

7) income in the form of interest, with the exception of interest on debt securities, received from:

residents;

nonresidents with a permanent establishment or property located in the Republic of Kazakhstan, if the debt owed by these nonresidents applies to their permanent establishment or property;

8) income in the form of interest on debt securities, received from:

resident issuers;

nonresident issuers with a permanent establishment or property located in the Republic of Kazakhstan, if the debt owed by these nonresidents applies to their permanent establishment or property;

9) income in the form of royalties received from residents or nonresidents in connection with doing business in the Republic of Kazakhstan through a permanent establishment;

10) income from the leasing of property located in the Republic of Kazakhstan;

11) income earned from real property located in the Republic of Kazakhstan;

12) income in the form of insurance premiums paid under agreements for the insurance or reinsurance of risks arising in the Republic of Kazakhstan;

13) income from providing transportation services for international shipments, one of the parties of which is the Republic of Kazakhstan;

14) income from operations in the Republic of Kazakhstan under individual labor agreements (contracts) or under other agreements of a civil-legal nature;

15) honoraria for managers and/or other payments received by members of a top administrative body (council of directors, board, or other similar body) of a resident legal entity, regardless of where the actual performance of the administrative duties assigned to such persons takes place;

16) supplemental payments made in connection with residing in the Republic of Kazakhstan;

17) income in the form of compensation for expenditures borne by an employer to provide material and social benefits or other material advantages to nonresident individuals working in the Republic of Kazakhstan, including expenditures on meals, housing, enrollment of children at educational institutions, and expenses related to leisure activities, including vacation travel for their family members;

18) pension payments effected by resident pension savings funds;

19) income paid to people employed in the arts: theater, film, radio and television performers, musicians, artists, and athletes from activities in the Republic of Kazakhstan, regardless of the person to whom payments are made;

20) winnings paid by residents;

21) income earned from providing independent personal (professional) services in the Republic of Kazakhstan;

22) income in the form of property located in the Republic of Kazakhstan that is received free of charge, including income from such property;

23) other income not covered under the preceding subitems that arises on the basis of activities performed in the Republic of Kazakhstan.

2.4 PROCEDURE FOR THE TAXATION OF INCOME EARNED BY NONRESIDENT LEGAL ENTITIES DOING BUSINESS WITHOUT CREATING A PERMANENT ESTABLISHMENT IN THE REPUBLIC OF KAZAKHSTAN

Income earned by a nonresident legal entity that defined above that is not related to a permanent establishment in the Republic of Kazakhstan shall be subject to the income tax at the source of payment without any deductions, at the rates set below.

Rates for the income tax at the source of payment

The income of a nonresident from sources in the Republic of Kazakhstan not related to a permanent establishment shall be subject to taxation at the source of payment at the following rates:

| 1) dividends, income from a share interest, and interest income |

15 percent |

| 2) insurance premiums paid under agreements for the insurance of risks |

10 percent |

| 3) insurance premiums paid under agreements for the reinsurance of risks |

5 percent |

| 4) income from providing transportation services in international shipments |

5 percent |

| 5) income defined under Article 178 of Tax Code of RK, with the exception of income referred to in subitems 1)–4) of this article |

20 percent |

The payment of income shall be defined as the mean the transfer of money in cash and/or noncash form, securities, goods, property, and the performance of work or delivery of services. The following shall not be subject to taxation at the source of payment:

1) payments related to the delivery of goods onto the territory of the Republic of Kazakhstan under foreign trade transactions;

2) income from providing services related to the opening and maintenance of correspondent accounts of resident banks and the performance of settlements on them;

3) capital gains from the realization of securities;

4) income from operations with government securities;

5) payments related to an adjustment, based on quality, in the selling price of crude oil transported via the unified pipeline system outside the Republic of Kazakhstan;

6) interest accumulated (accrued) on debt securities paid by resident buyers (not issuers) to nonresidents at the time of their purchase.

The taxation of a nonresident’s income at the source of payment shall be effected regardless of whether said nonresident turns over this income to third parties and/or to its subdivisions in other states. The procedure for the calculation and withholding of income tax at the source of payment from interest on debt securities shall be established by the authorized government agency. The person paying income (including a nonresident doing business in the Republic of Kazakhstan through a permanent establishment) is liable and responsible for the calculation and withholding of the income tax at the source of payment, and for payment of the tax to the state budget. Such a person shall be recognized as a tax agent in accordance with item 1 of Article 10 of Tax Code. A nonresident shall be recognized as a tax agent as of the moment said person begins doing business in the Republic of Kazakhstan, if its period of operation exceeds that established for the creation of a permanent establishment. The income tax shall be withheld at the source of payment regardless of the form and place of payment of the income.

2.4.1 Procedure and deadlines for the payment of income tax at the source of payment

Income tax withheld from the income of a nonresident legal entity at the source of payment shall be payable to the state budget:

1) on the amount of income paid – within five business days of the end of the month in which payment was effected;

2) on the amount of income accrued but not paid, when the income is taken as a deduction, within ten business days of the deadline established for the filing of a corporate income tax return.

The provision of this subitem shall not extend to interest on debt securities, the maturities of which fall after expiration of the deadline established by this subitem.

Tax agents shall be required to file a statement of income tax withheld at the source of payment with tax authorities where they are registered, on a quarterly basis no later than the 15th

of the month following the reporting quarter in which an obligation to withhold income tax at the source of payment occurred.

2.4.2 Provisions specific to the calculation and payment of income tax on capital gains from the realization of securities

A nonresident’s income from capital gains resulting from the realization of securities issued by residents shall be subject to taxation at the rate established under Article 180 of Tax Code, with the exception of capital gains from the realization of stocks and bonds that are on the stock exchange’s official “A” and “B” lists. The corporate income tax shall be calculated independently by the nonresident legal entity, the tax shall be payable within ten business days of the moment at which the income was received, and the filing of a corporate income tax return with the tax authority where the issuer is registered shall be required.

2.5 PROCEDURE FOR THE TAXATION OF INCOME OF NONRESIDENT LEGAL ENTITIES DOING BUSINESS IN THE REPUBLIC OF KAZAKHSTAN THROUGH A PERMANENT ESTABLISHMENT

The procedure for determination of the taxable income, and for the calculation and payment of the corporate income tax on a nonresident legal entity doing business in the Republic of Kazakhstan through a permanent establishment, shall be carried out in accordance with the provisions of Articles 79–135 of Tax Code of RK.

The income of a nonresident legal entity shall include all types of income related to the operation of the permanent establishment.

If a nonresident legal entity does business in the Republic of Kazakhstan that is analogous or similar to that which is performed through a permanent establishment, the income from that business shall be treated as income from doing business through the permanent establishment.

Expenses related directly to earning income from doing business in the Republic of Kazakhstan through a permanent establishment shall be deductible, regardless of whether they were incurred in the Republic of Kazakhstan or outside its borders, with the exception of expenses that may not be taken as a deduction in accordance with this Code.

A nonresident legal entity shall not have the right to deduct the following amounts charged to a permanent establishment in the form of:

1) royalties, honoraria, fees, and other payments for the use of or granting the right to use property or intellectual property of the given nonresident legal entity;

2) commission income for services;

3) interest on loans granted by the given nonresident legal entity;

4) expenditures not related to earning income from the nonresident legal entity’s operations in the Republic of Kazakhstan;

5) expenditures that are not documented;

6) management and general administrative expenses of the nonresident legal entity incurred outside the territory of the Republic of Kazakhstan.

2.5.1 Procedure for taxation of the net income of a nonresident legal entity from doing business through a permanent establishment

The net income of a nonresident legal entity from doing business in the Republic of Kazakhstan through a permanent establishment shall be subject to taxation at the rate of 15 percent. (Net income shall be understood to mean taxable income, less the amount of corporate income tax assessed.) The amount of tax assessed on net income shall be reflected in the corporate income tax return.

A nonresident legal entity shall be required to pay the tax on net income from doing business through a permanent establishment within ten business days of the deadline established for the filing of the corporate income tax return.

2.5.2 Procedure for taxation of the income of a nonresident legal entity in certain cases

The income of a nonresident legal entity that is not registered with a tax authority, which it has earned from doing business in the Republic of Kazakhstan through a permanent establishment, shall be subject to the income tax at the source of payment without any deductions.

The income tax withheld at the source of payment by a tax agent shall be credited against the discharge of the tax obligations of a nonresident doing business through a permanent establishment.

2.6 PROCEDURE FOR TAXATION OF THE INCOME OF NONRESIDENT INDIVIDUALS

The income of a nonresident individual, as defined above, which is not related to a permanent establishment of said individual, should be subject to taxation at the source of payment following the procedure and within the deadlines specified by the provisions of Articles 179–181 of Tax Code of RK, with the exception of:

1) income from individual entrepreneurial activity through a permanent establishment in the Republic of Kazakhstan;

2) interest on bank deposits;

3) payments related to the delivery of goods onto the territory of the Republic of Kazakhstan under foreign trade transactions;

4) capital gains from the realization of securities;

5) income from operations with government securities;

6) interest accumulated (accrued) on debt securities at the time of their purchase, paid by resident buyers (not issuers) to nonresidents.

The obligation and responsibility for the calculation and withholding of the income tax at the source of payment, and for payment of the tax to the state budget, shall be assigned to the person paying the income (including a nonresident doing business in the Republic of Kazakhstan through a permanent establishment). Such a person shall be recognized as a tax agent in accordance with item 1 of Article 10 of Tax Code of RK.A nonresident shall be recognized as a tax agent as of the moment said person begins doing business in the Republic of Kazakhstan, if its period of operation exceeds that established for the creation of a permanent establishment. The income tax shall be withheld at the source of payment by a tax agent regardless of the form and place of payment of the income.

Filing of tax reports

Tax agents shall be required to file a statement of income tax withheld at the source of payment with tax authorities where they are registered within the deadlines established under Article 182 of Tax Code of RK.

2.6.1 Procedure for calculation and payment of the income tax on a nonresident individual whose activities lead to the creation of a permanent establishment

A nonresident individual who is engaged in individual entrepreneurial activity in the Republic of Kazakhstan through a permanent establishment shall be a payer of the individual income tax with regard to income related to said activity, less deductions directly tied to this income, with the exception of expenses that are not deductible in accordance with item 5 of Article 184 and the provisions of Tax Code. Dependent personal services (work for hire) provided by a nonresident individual shall not lead to the creation of a permanent establishment of said individual.

2.6.2 Procedure for the taxation of a nonresident individual’s income in certain cases

The income earned by a nonresident individual from sources in the Republic of Kazakhstan that is not subject to the income tax at the source of payment and that is not related to a permanent establishment of said individual, including capital gains from the realization of securities issued by residents, shall be subject to taxation, without taking any deductions, at the rates established under Article 180 of Tax Code. Capital gains from the realization of stocks and bonds that are on the stock exchange’s official “A” and “B” lists shall not be subject to taxation. The calculation and payment of the individual income tax shall be performed by a nonresident individual independently within the deadlines established under item 5 of Article 191 of Tax Code.

2.6.3 Procedure and deadlines for prepayment of the individual income tax

The following nonresident individuals shall pay the individual income tax by making prepayments:

1) nonresident individuals earning income from individual entrepreneurial activity in the Republic of Kazakhstan through a permanent establishment;

2) nonresident individuals earning income defined under subitems 14)–17) of Article 178 of Tax Code, including other income defined under Articles 149–151 of Tax Code, with the exception of income subject to the income tax at the source of payment.

Prepayments of the individual income tax for the period of operation shall be made by a nonresident individual mentioned above, following the procedure and within the deadlines established by Tax Code. The amount of prepayments of the individual income tax, which are payable in equal installments during the period that a nonresident is doing business in the Republic of Kazakhstan, shall be determined on the basis of the amount of tax indicated in a statement of the anticipated amount of individual income tax. Nonresident individuals referred to in subitem 2) shall be required to attach to the statement of the anticipated amount of individual income tax an individual labor agreement (contract) or other agreement of a civil-legal nature confirming the declared amount of taxable income. Prepayments that are made shall be credited against the payment of the individual income tax owed by a nonresident individual for the current tax period. A final settlement and payment of individual income tax shall be effected within ten business days of the date an individual income tax return for the tax period is filed, but not later than ten business day prior to departure from the Republic of Kazakhstan.

2.6.4 Statement of anticipated individual income tax and individual income tax return

Nonresident individuals referred to in Article 191 of Tax Code of RK shall be required to file with tax authorities serving the area where they are staying a statement of the anticipated amount of individual income tax for the period they are in operation, no later than 30 business days from the date of their arrival in the Republic of Kazakhstan. The following nonresident individuals shall file an individual income tax return with tax authorities serving the area where they are staying within the deadline established under Article 172 of this Code, or in the event of the termination of their entrepreneurial activity and their departure from the Republic of Kazakhstan during the current tax period, no later than ten business days prior to their departure:

those earning income from sources in the Republic of Kazakhstan that is not subject to the income tax at the source of payment;

those engaged in entrepreneurial activity in the Republic of Kazakhstan for more than 30 calendar days or earning income from sources in the Republic of Kazakhstan in excess of 500 times the monthly index factor during the tax period.

2.7 SPECIAL PROVISIONS REGARDING INTERNATIONAL AGREEMENTS

The Tax Code of RK gives provisions of an international agreement to avoid dual taxation and prevent evasion of taxation of income or property (capital) to which the Republic of Kazakhstan is a party (referred to hereinafter as an international agreement for the purposes of Articles 193–204 of Tax Code of RK) shall apply to persons who are residents of one or both of the states that have concluded such an agreement. This statement does not extend to a resident of a state with which an international agreement has been concluded if this resident uses the provisions of the international agreement in the interests of another person who is not a resident of a state with which an international agreement has been concluded. The administration of international agreements shall be carried out following the procedure established by the authorized government agency in accordance with the provisions of Articles 193–204 of Tax Code.

If the provisions of an international agreement regarding the determination of taxable income of a nonresident legal entity from doing business in the Republic of Kazakhstan through a permanent establishment allow for the deduction of management and general administrative expenses incurred for the purpose of earning said taxable income both in the Republic of Kazakhstan and outside its borders, one of the following methods shall be used to determine these expenses:

1)

The proportional distribution of expenses method;

2)

The direct deduction of expenses method.

A nonresident legal entity may choose for itself one of these methods for the deduction of management and general administrative expenses. The method chosen for the deduction of management and general administrative expenses charged to a permanent establishment (including the procedure for calculation of the index factor used in the proportional distribution of expenses method) shall be applied annually and may be changed only with the approval of a tax authority.

2.7.1 Proportional distribution of expenses method

When the proportional distribution of expenses method is used, the amount of management and general administrative expenses referred to in Article 195 of Tax Code of RK that are charged to a permanent establishment as a deduction shall be determined as the product of these expenses and the index factor. The index factor shall be calculated by one of the following methods:

1) the ratio of gross annual income earned by a nonresident legal entity from doing business in the Republic of Kazakhstan through a permanent establishment during the tax period to the total gross annual income of the nonresident legal entity as a whole for the same tax period;

2) the average of the following three indicators:

the ratio of gross annual income earned by a nonresident legal entity from doing business in the Republic of Kazakhstan through a permanent establishment during the tax period to the total gross annual income of the nonresident legal entity as a whole for the same tax period;

the ratio of the value of fixed assets recorded in the financial statement of the permanent establishment in the Republic of Kazakhstan as of the end of the tax period, to the total value of the fixed assets of the nonresident legal entity as a whole in the same tax period;

the ratio of the wages fund for personnel employed at the permanent establishment in the Republic of Kazakhstan as of the end of the tax period to the wages fund for personnel of the nonresident legal entity as a whole in the same tax period.

A nonresident legal entity can determine independently which of the aforementioned methods for calculation of the index factor will be used.

The amount of management and general administrative expenses arrived at through these calculations shall be taken as a deduction charged to the permanent establishment only if supporting documents are available. Supporting documents shall include:

1) a copy of the financial statements of the nonresident legal entity in which the following is indicated, depending on the index factor chosen by the nonresident legal entity:

the total amount of gross annual income as a whole;

the total amount of the wages fund as a whole;

the original and residual value of fixed assets as a whole;

the total amount of expenses, with an item-by-item breakdown, including a breakdown of the total amount of management and general administrative expenses;

2) a copy of an audit opinion based on an audit of the nonresident legal entity’s financial statements (if an audit of the legal entity’s financial statements has been performed).

A statement of the aforementioned expenses that are taken, as a deduction charged to a permanent establishment in the Republic of Kazakhstan shall be attached to the corporate income tax return filed with the appropriate tax authority of the Republic of Kazakhstan. In the event that the amount of management and general administrative expenses subject to proportional distribution is not indicated in the financial statements, these expenses shall not be taken as deductions charged to a permanent establishment.

2.7.2 Direct deduction of expenses method

When the direct deduction method is used for a nonresident’s management and general administrative expenses, these expenses shall be taken as a deduction charged to a permanent establishment in the Republic of Kazakhstan if they can be determined directly and were incurred directly for the purposes of earning income from doing business in the Republic of Kazakhstan through a permanent establishment. Said expenses shall be taken as deductions charged to a permanent established only if supporting documents are available. Supporting documents shall include:

1) accounting records confirming expenses incurred by the nonresident legal entity on the territory of the Republic of Kazakhstan for the purposes of earning income from doing business through the permanent establishment;

2) copies of accounting records confirming expenses incurred by the nonresident legal entity outside the Republic of Kazakhstan for the purposes of earning income from doing business in the Republic of Kazakhstan through the permanent establishment.

2.7.3 Procedure for payment of the income tax on income earned by nonresidents from activity in the Republic of Kazakhstan not leading to the creation of a permanent establishment

The procedure for payment of the income tax provided for under this statement shall apply to the income of a nonresident from activity in the Republic of Kazakhstan that does not lead to the creation of a permanent establishment in accordance with the provisions of an international agreement, with the exception of income referred to in Articles 199–202 of Tax Code Of RK, except as otherwise provided under said statements. A nonresident mentioned above of this article that earns income from sources in the Republic of Kazakhstan shall have the right to apply the procedure for payment of the income tax provided for under this article. In the event that the provisions of this article are not applied, a tax agent shall be required to withhold the income tax at the source of payment and transfer it to the state budget in accordance with the generally established procedure. A nonresident earning income, a tax agent, and a resident bank (referred to hereinafter as a bank) identified by a tax agent, shall conclude a conditional bank deposit agreement following the form agreed upon by the parties to the agreement, taking into account the provisions of this article. Within ten business days of the signing of a conditional bank deposit agreement, a tax agent shall be required to register the agreement with a tax authority, and a copy of the agreement, as well as a copy of the payment document confirming the transfer of income tax to a conditional bank deposit, shall be submitted to the tax authority. The provisions of this article shall extend only to conditional bank deposit agreements that have been registered with a tax authority. Conditional bank deposit agreements, the terms of which do not contradict the provisions of this article, shall be subject to registration. At the time income is paid to a nonresident, a tax agent shall be required to withhold income tax at the source of payment at the rate specified under Article 180 of Tax Code, and to transfer the tax that has been withheld to the conditional bank deposit at a bank, in favor of the nonresident. In the case of compliance with the terms of an international agreement, in order to obtain a refund of income tax that has previously been withheld, a nonresident shall file a request with the tax authority following the procedure and form established by the authorized government agency.. The tax authority shall review said request and the required documents, it shall make a decision regarding the request, and it shall notify the nonresident and the bank of the decision. Upon receipt of a request for a refund of income tax that has been withheld, which has been certified by a tax authority, a bank shall grant the nonresident who submitted the request the right to dispose of funds placed in the conditional bank deposit, up to the amount indicated in the request, plus bank interest that has accrued. In the event that a nonresident does not agree with a negative decision by the tax authority, the nonresident shall have the right within ten business days of the receipt of such a decision to file a request with the authorized government agency (with the involvement of the competent authority of the nonresident’s country of residence, if necessary), asking that the matter be reviewed again to determine the proper application of the provisions of the international agreement, and the tax authority shall be notified at the same time of the appeal of its decision. In the event that a negative decision is made regarding a request and if no notification of an appeal of the tax authority’s decision is received from a nonresident within the established deadline, within ten business days of the nonresident’s receipt of the refusal to apply the provisions of an international agreement, the tax authority shall forward a collection order to the bank calling for transfer of the amount indicated in the request and placed in a conditional bank deposit, plus bank interest that has accrued, to the state budget, accompanied by a document confirming the refusal to exempt the nonresident from taxation. A bank shall be required, within one business day of the receipt from the tax authority of documents referred above, to transfer the amount of income tax placed in the conditional bank deposit, plus bank interest that has accrued, to the state budget. The amount of tax collected shall be credited against the nonresident’s obligations to the state budget. Conditional bank deposits shall be opened in the national currency or in a foreign currency. In the event that conditional bank deposits are opened in a foreign currency, the income tax and bank interest shall be transferred to the budget in the national currency, after being converted at the official rate of the National Bank of the Republic of Kazakhstan at the time the tax is paid. A nonresident and a tax agent shall not have the right to dispose of income tax placed in a conditional bank deposit until a decision of some kind is reached by the tax authority. In the event that the terms of a conditional bank deposit agreement are violated and income tax that has been withheld is not transferred to the state budget in a timely manner, through the fault of the bank, the bank shall bear liability in accordance with legislative acts of the Republic of Kazakhstan. If it is not possible for a bank to meet its obligations to transfer income tax placed in a conditional bank deposit to the state budget, the obligation to transfer income tax collected at the source of payment, bank interest, and fines for the late transfer of tax to the state budget shall be assigned to the tax agent. Tax authorities shall be required to maintain a record of the amount of income tax:

1) placed in conditional bank deposits;

2) paid to nonresidents who have the right to apply the provisions of international agreements;

3) transferred to the state budget.

2.7.4 Procedure for the application of an international agreement with respect to taxation of income from providing transportation services in international shipping

Income from providing transportation services in international shipping in which the Republic of Kazakhstan is one of the parties, earned by a nonresident legal entity that has the right to apply the provisions of an international agreement, shall be exempt from taxation without the filing of a request for application of the provisions of the international agreement, on the basis of a document confirming residency, if the legal entity has a permanent establishment in the Republic of Kazakhstan that is related to this activity. In this case the nonresident legal entity shall be required to maintain a separate record of income earned from providing transportation services in international shipping (which is not subject to taxation pursuant to an international agreement) and from providing transportation services on the territory of the Republic of Kazakhstan (subject to taxation), and also to reflect said income in a corporate income tax return. The total amount of taxable income indicated in a corporate income tax return shall be reduced by the amount of taxable income that is exempt from taxation pursuant to an international agreement, calculated on the basis of the separate accounting records. In the event of the unlawful application of the provisions of an international agreement, which results in nonpayment, or incomplete payment of tax to the state budget, the taxpayer shall bear liability in accordance with legislative acts of the Republic of Kazakhstan.

Income earned by a nonresident legal entity that has the right to apply the provisions of an international agreement, from the operation of means of transport in international shipping in which the Republic of Kazakhstan is one of the parties, without the creation of a permanent establishment in the Republic of Kazakhstan, shall be exempt from taxation in accordance with the procedure established under Article 198 of Tax Code.

2.7.5 Procedure for the application of an international agreement with regard to the taxation of dividends, interest, and royalties

At the time that income is paid to a nonresident in the form of dividends, interest, or royalties, a tax agent shall have the right to apply the provisions of the respective international agreement without the filing by the nonresident of a request for application of the provisions of an international agreement, on the basis of a document confirming residency, if the nonresident in question is the final recipient of the income and has the right to apply the provisions of an international agreement. A tax agent shall be required to indicate in the statement of income tax collected at the source of payment which is filed with a tax authority the amount of income paid (accrued) and taxes withheld in accordance with the provisions of international agreements, the income tax rates, and the names of the international agreements. In the event of the unlawful application of the provisions of an international agreement which results in nonpayment or incomplete payment of tax to the state budget, the tax agent shall bear liability in accordance with legislative acts of the Republic of Kazakhstan.

2.7.6 Procedure for the application of an international agreement with regard to the taxation of net income from doing business through a permanent establishment

A nonresident shall have the right to apply the provisions of an international agreement with regard to the taxation of net income from doing business in the Republic of Kazakhstan through a permanent establishment without filing a request for application of the provisions of an international agreement, on the basis of a document confirming residency, if the nonresident in question is the final recipient of the net income and has the right to apply the provisions of the respective international agreement. A nonresident legal entity shall be required to indicate in a corporate income tax return the tax rate, the amount of tax on net income, and the name of the international agreement on the basis of which the respective tax rate was applied. In the event of the unlawful application of the provisions of an international agreement which results in nonpayment or incomplete payment of tax to the state budget, the taxpayer shall bear liability in accordance with legislative acts of the Republic of Kazakhstan.

2.7.7 Procedure for the application of an international agreement with regard to the taxation of other income from sources in the Republic of Kazakhstan

A nonresident earning income from sources in the Republic of Kazakhstan, with the exception of those referred to in Articles 198–201 of Tax Code, shall have the right to file a request to apply the provisions of an international agreement, following the form established by the authorized government agency, with the tax authority where the tax agent is registered, prior to the payment of the income. A tax authority shall review the request, and if the information indicated in the request is valid, it shall certify the request as filed.In the event of the unlawful application of the provisions of an international agreement, the tax authority shall deny the request and inform the nonresident of its reasons for doing so. In the event that a nonresident does not agree with a tax authority’s negative decision, the nonresident shall have the right to file a request with the authorized government agency (with the involvement of the competent authority of the nonresident’s country of residence, if necessary), asking that the matter be reviewed again to determine the proper application of the provisions of the international agreement.