Oligopoly is a market structure under which only a few suppliers dominate the market and the entrance of new suppliers is either constrained or impossible.[1]

Usually, the oligopoly market is dominated by 2-10 firms, who have a joint share of the market of 50% or more. Automobile, steel, air transport are common examples of oligopolies. Or, in a global sense, we could call oil producer countries oligopolies and OPEC – a cartel. At least some firms may influence price due to their important contribution to the total output. Every firm in the situation of oligopoly knows that if it, or its competitors either change prices or output, the revenues of all the participants on the market will change. That means that firms are interdependent. For example, if General Morors Corporation decides to raise prices on its cars, it should consider retaliative moves by Ford, Chrysler, and other competitors in order to calculate the ultimate changes in sales.

It is generally assumed that every firm on the market realizes that its changes in prices or output will cause other firms to retaliate. The kind of retaliation any supplier expects from its competitors as a reaction to his changes in prices, output, or change of marketing strategy is the main factor that influences its decisions[2]

. That expected reaction also influences the balance of oligopoly markets.

Oligopolies may interact in two main ways:

1) Price wars, when a firm tries to increase it sales by reducing prices, expecting that other firms will not be able to respond by doing the same. This stops when no firm can low its prices anymore, which occurs when P=AC and profit equals 0. Unfortunately for consumers, price wars do not usually last long. Firms have temptations to co-operate with each other in order to set up higher prices and to share markets in such a way, as to avoid new price wars and their bad impact on revenues.

2) From the above factor results co-operation. Its closest form is a cartel, when a union of oligopolies acts as a monopoly. Cartels are illegal in many countries of the World.

Another reason for co-operation is to increase the entrance barriers to prevent other firms (especially the so-called hit and run firms

) to join the market and drop prices. In that situation firms try to coordinate their activities.

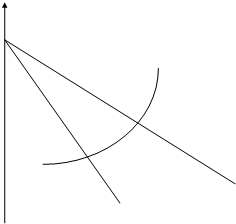

To answer this question, I first need to describe the way agreement between oligopolies form. Let us suppose that there are 15 suppliers in the area A who want to co-operate with each other. These firms set their prices equal to their average costs. Each of the firms is afraid to raise prices for the reason its competitors might not follow that move and its profits will become negative. Let us suppose that the production is at the competitive level Qc

(pic. A), that corresponds to the production quantity under which the demand curve crosses MC, which is a horizontal sum of the marginal cost curves of each supplier. MC would coincide with the demand curve if the market were perfectly competitive. Each firm produces 1/15 of the total output Qc

.

Реклама

Pic. А

Pm Pm

Pc E Pc E

MR` MR`

MC D

MR

Qm Qc Q`

The original balance exists at the point E.; the competitive price is Pc. At that price each of the producers gets normal revenue. At the price Pm, resulting from the co-operation agreement, each firm could maximize its profits by setting Pm=MC. If each of the firms does that, than there will be an over supply on the market, equal to QmQ units per month. The price would fall to Pc. In order to maintain cartel price, each of the firms should produce no more than the quota qm.

When the firms decide to co-operate, they should implement the following policies to be able to maximize their profits.

1) They should make sure that there exists an entrance barrier to the market in which they operate in order to prevent other firms from selling a good at an old price after they increase prices for their output. If the barriers do not exist, then the increase in prices would attract other producers. The supply would then increase and prices would fall below the monopoly level, co-operating firms aim to maintain.

2) They should decide on the general pattern of production. This could be done by estimating market demand and by calculating marginal profit for all levels of production. Firms need to produce so that their MC=MR (we assume that all firms have similar production costs). The monopoly production level would maximize revenues of each of the firms (see Pic. A). The demand curve for the output is in the region of D. The marginal revenue that corresponds to that curve is MR. The monopoly production level equals to Qm, which corresponds to the point where MR crosses MC. The monopoly price equals Pm. The current price equals Pc and the current output – Qc. That means that the current balance is the same as it would be under competition.

3) Each participant in co-operation agreement should have production quotas. The monopoly production Qm should be divided between all members of the treaty. For example, each firm could produce a 1/15 share of Qm per month. If all the firms had identical cost functions it would be equivalent to recommending them to balance their production till their marginal costs become equal to the market marginal revenue (MR’). Until the sum of the monthly outputs of all producers equals Qm, it is possible to maintain the monopoly price.

Firms under co-operation agreement usually encounter problems when they try to make a decision about monopoly prices and the level of output. These problems are especially serious if the firms cannot agree on the estimate of the market demand, its price elasticity; or, if they have different production costs.[3]

Firms with higher production costs try to insist on higher prices.

Реклама

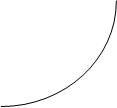

Every firm has incentives to increase its production at cartel prices. At the same time, if everyone will increase production then the agreement will fail because prices will decrease to their initial level. Pic. B shows marginal and average costs of a typical producer. Before the conclusion of co-operation agreement the firm behaves as if the demand for its output at the price Pc was perfectly elastic. It does not increase prices because it fears to lose all its sales to its competitors. It produces the quantity qc. As all firms behave in the same way, the industrial output equals Qc, which is the value that would exist under perfect competition. Under the newly established agreed prices the firm is allowed to produce qm units of output, corresponding to the point at which MR equals MC of each of the firms.

Pic. В

AC MC AC MC

Pm A F Pm A F

C B C B

H G H G

MR` MR`

qm qc q`

Let us suppose that the owners of any one of the firms think that the market price will not fall if they start selling more than that quantity. If they take Pm as price lying beyond their influence, then their profit maximizing output will be q’, under which Pm=MC. If the market price does not decrease, the firm can increase its profits from PmABC to PmFGH by producing above the quota.

Just one firm could be able to increase its output without causing any significant decrease in market prices. Let us suppose, however, that all producers start producing above their quotas in order to maximize their profits under “cartel”[4]

prices Pm. The industrial output would then increase to Q’, under which Pm=MC, which will result in excess supply as at that price the demand would be lower than the supply. Consequently, prices will fall until the market clears, i.e. till they become equal to Pc and the producers will come back where they have initially started.

Cartels usually try to penalize those who cheat with quotas. The main problem however occurs when the cartel price gets set up, some firms, aiming to maximize their profits, could earn more by cheating. If everyone is cheating the co-operation agreement breaks down as profits fall to 0.

1. Grebenschikov P.I., Leusskiy A.I., Tarasevitch L.S, Microeconomics

,

St. Petersburg 1996., pp. 213- 216

2. Livshits A.Y. Introduction to the Market Economy

, Moscow 1991, pp.158-161

3. McConnell C.P., et al., Economics

, Moscow 1993, pp. 125-7

4. Begg D., Fisher S., Dornbusch R., Economics

, 5th

ed., McGraw-Hill 1997, pp. 151-51, 176, 146, 148

5. Lancaster K., Introduction to Modern Microeconomics

, 2nd

ed., N-Y 1974, p. 200-1

6. Nicholson W., Microeconomic Theory

, 7th

ed., The Dryden Press 1998, pp. 580-4

[1]

Grebenschikov P.I., Leusskiy A.I., Tarasevitch L.S, Microeconomics

,

St. Petersburg 1996., p. 213

[2]

Livshits A.Y. Introduction to the Market Economy

, Moscow 1991, p.159

[3]

Livshits A.Y. Introduction to the Market Economy

, Moscow 1991, p. 161

[4]

I am using the expression “cartel price” for the purpose of simplification. What I mean by it is the high price that resulted from the co-operation agreement between oligopolies.

|