| PLAN

The Introduction

I. The Banking System of the United State of America

1) Central Banking

2) Commercial Banking and the Development of the Fed

3) The Federal Reserve and Monetary Policy

4) Depository Institutions: Commercials Banks and Banking Structure

II. The Banking System of Ukraine

1) Banking System in Transition

2) Role of the National Bank of Ukraine

The Introduction

The modern world system of the central bank was created relative recently.Until to middle 18 century commercial and central banks did not differ. With the development of credit system there is a process of centralization banknote issues in some of commercial banks. Thus the monopoly rights on issues of banknotes gradually fixed only to one bank. Such bank in differen time called differently. First – national , and then central , that answered its managing role in credit system of the certain country.

The first central bank was created in Sweden (Rixbank) in1668.Later ,1694 was founded the Bank of England. But on that time central banks had not rights on banknotes issues .Their functions differ from functions of modern central banks. For example , the main role of the Bank of England was financing the trade and industry ,the first role of the Bank of Holland – domestic and international trade .The central banks as a modern types appeared only in 19 century. Now , in many countries of the world has a central bank : the Federal Reserve System in the USA , the Bank of Japan,etc. But all of them differ from each other , because there are political and financial differs between the countries.

In 20 century allocation in banking system central level in many advanced countries of the world is not only natural phenomenon , but also an obligatory condition of achievement of high economic development.

The legal status of central banks , their status in the advanced countries is determined by the legislation.In many countries the basic act which regulates activity of the centralbanks , the act of the supreme validity is the law. In law about the banks their structure, the basic tasks , function and the competence, the order of relations with bodies of legislative and executive authority , the state controls is determined.In legal acts which determine the status of central banks , their dutiesin spheres of management of monetary circulation, currency transaction , functioning of credit system will be worn out.

Реклама

On a pattern of ownership central banks can be state or join-stock. For example , in France, UK, German , Spain the capital completely belongs to the state. In some countries the state owns a part of the capital (Belgium , Japan) .In the USA shareholders of the central bank (Federal reserves banks) are only commercial banks. Therefor , in any case the state plays a leading role in formation of controls of central bank.

There are two models of mutual relation between cental banks and ixisting branches of authority. The first – central bank is the agent of the government and a conductor of its credit policy. The second – central bank is independent of the government that provides independence in realization of a monetary and credit policy without influence from the side of governmental bodies. But in practice these models in "a pure kind " do not function.In most countries there are intermediate models.

The legislation only 5 countries – USA , Germany , Sweden , Holland , Suice – provides submission of central banks to the government. In most countries of the world the central banks submit to exchecuer or to the ministry of finance.

In legislation of UK, France, Italy, Japan and some others countries is provided, that ministry of finance has the right to give out the instruction to the central banks. But such cases are very rare.

In the countries where legislation acts submission of central banks directly to parlaments is stipulared , with the help of the certain procedures are possible acceptance of decisions with wich regulatory authorities undertake to promote central banks in the decision of the certain problems , in fulfilment of a monetary and credit policy. Except for it , the legislation of some counties provides the reporting central banks before parlaments. For example , Federal Reserve System gives to the Congress of USA the report about the activity two times per one year . Central bank of Germany and Japan give report in the parlament annually.

Central banks in the majorityof the countries of the world constantly are supported support of the state . Central banks are capable to register all payment operations , qualitatively to carry out tranxfer mutual duties of bank. Central bank makes macroeconomic supervision , the control of functioning of all bank system , and also of activity of each bank separately.

Реклама

The role of central bank is different countries is not identical. In particular , the big value plays a skill level of participants of payment attitudes , wich will carry out depository operations. There are differences both in legal base and in approaches of the different states to fulfilment by subjects of the market financial activity.

What about federal Reserve System of the USA you can read in the next chapter.

I. The Banking System of the United State of America

1) Central Banking

The banking system of the United States of America consists of the Federal Reserve System,commercial banks,savings and loans associatios,mutual savings banks,and credit unions.

The Federal Reserve System (the Fed) is the central bank of the United States.It was established in 1913 to promote a healthy economic climate that banks in financial difficulties by providing limited crsdit facilities. A central bank is often thought of a bankers’ bank,overseeing the banking system.The central bank also is usually the goverment ’s bank and conducts monetary policy in major developed countries .The Fed has a number of responsibilities,many involving the commercial banking system directly.These include regulating a major portion of the system and leading funds as required to all commercial banks and many other depository financial intermediaries.The Fed ’s influense on commercial banking in particular and on the whole financial system.The Federal Reserve System also provides federal insurance to commercial bank-members of insurance scheme.If these banks go bankrupt,their depositors will receive a compensation of up to 100,000 dollars for each account they had.

Commercial banks can be thought of as the hub of the financial system.They are difined by federal statutes as an entity that accept demand deposits and makes commercial loans.They account more than 60 percent of all deposits in the United States.Commercial banks’ lending activity is also substantial.For example,the banks had almost $650 billion in commercial and industrial loans and $756 billion in mortgage loans outstanding at the end of 1989.They were by far the lagest lenders to bussiness and the second largest mortgage lenders after savings institutions.In recent years , they have surpassed savings institutions in mortgage lending in many periods.

2) Commercial Banking and the Development of the Federal Reserve System

Commercial banks in the United States include money centres,regional,local and foreign banks.Their operations are generally similar to those of banks in other countries.

One of the specific characteristics of American banks is that they cannot own securities for their own account exept in the case of foreclosure on a defaulted loan.Another particular requirement to the activities of commercial banks is that they must distinguish their commercial activities from their trust activities,i.e. information obtained by one bank department cannot be transmitted to the another one.

When funds deposited into a demand deposit or checkable deposit account at a commercial bank,they are immediately available on demand.Checks can be written on the account and are honored by the bank on presentation.However,the bank does not hold the funds on deposit until the check is written.Banks are business and the goal of their operations is to make a profit.Therefore, they must make use of the funds deposited with them , primarily by making loans and purchasing securities.How funds on deposit can be used for lending and at the same time be available on demand requires an understanding of fractional reserv banking.

Fractional Reserve Banking

Banks in some form have existed since ancient times.Modern banking traces its origins to Italy during the Renaissance,and to London,where the first fully operationl commercial bank was established in 1684.About 100 years later, in 1782, the first commercial bank was founded un the United States.

Like many other early commercial banks, the London bank was once a goldsmith shop.Sincr gold left for safekeeping generally stayed in storage (on deposit) for long periods of time, goldsmith found that they could meet withdrawal demands from new deposits of gold without touching the earlier deposits.The amount of gold on deposit continued to grow, due in part to the fact that the receipts issued by goldsmith to depositors were circulating as money; therefore, depositors did not require physical possession of their gold for transaction.The next step was that goldsmith found that they could profitably loan out much of the gold on deposit, or claims to to it in theform of receipts, without endangering their solvency.The issuance of several claims on a given amount of reserves (in this case gold) was the beginning of fractional reserve banking.

Fractional reserve banking means that banks do not keep 100 percent of deposit on hand as reserves.Rather only a fraction is held ,with the remainder used to acquire income-earning assets.The acceptability of bank notes (the goldsmiths’ receipts ) as money developed rapidly and led to the use of deposits as money throught written orders of payment (checks) that transferred ownership of gold or bak notes on deposit.

The principle of fractional reserve banking is still valid today.Most withdrawal demands from commercial banks are met from funds the banks receive the same day.Furthermore,since deposits have grown over the years , more funds have flowed into than out of banks on average.Only a small percentage of funds is kept on hand to meet contingencies , and banks can use the remainder to make loans and buy securities.

Commercial banks once decided throught trial and error on the proportion of deposits they should kssp in reserve , but not longer.In most Western countries this decision is make by the central bankor the goverment.In the United States,the Federal Reserve determines the reserve requirement withinlimits set by thr Congress.

Formation of the Federal Reserve System

The Fed was founded in 1913 as a direct outgrowth of the financial panic of 1907,which was the last in a series of such crieses that had occurred in 1873,1893,and 1903.After the 1907 panic,the Aldrich Commission,named for its chairman,was established to recommend a solution to these recurrent difficulties.The Commission recommendations were implemented in the Federal Reserve Act of 1913,creating the Fed as the central bank.The Federal Reserve System began operations in 1914.A central bank had not existed in the United States since President Andrew Jackson Refused to renew the charter of the Second Bank of the United States in 1836. Jackson believed that too much financial power was being concentrated in the northeastern United States.Although some of the traditional functions of a central bank were performed by the Treasury between 1836 and 1914,the financial panics and other problems clearly demonstrated that Treasury activities were no substitute for a fully functioning central bank.

The Federal Reserve Act charget the Fed with "providing an elastic currency" and acting as a "lender of last resort" to thr banking system.Essentially , it became a bankers’ bank;banks could borrow from the Fed when necessary to meet depositors’ increased demands for funds.It was hoped that the creation of the Fed would eliminate financial panics and lead to a more smoothly functioning financial system.The importence of providing an elastic currency can be appreciated by analyzing certain aspect of the demand ror money and credit in the economy.

Many times each year the economy has an increased need (demand) for money and credit.When this takes place om a regular basis, it is called a seasonal increase in demand.Typically , it occurs at Christmas,tax payment dates , and spring agricultural planting time (because farmers need money to buy seed and fertilizer).Nonregular , temporary increases in demand can occur at any time of year.Prior to creation of the Fed , these increased needs for money and credit occasionally could not be met by banks from their own reserves , and no central bank was available to which the commercial banks could turn.In severe cases financial panics ensued.

By standing ready to lend reserves to the banking system , the Fed ensures that banks can accomodate the needs of commerce under borth normal and abnormal conditions.As a result,the money supply can expand when pressure is applied and return to normal when it subsides.Providing such an elastic currency was at first the Fed’s main mission , its role has expanded enormously.

Today, the federal reserve’s duties fall into four general areas:

· Conducting the nation’s monetary policy by influencing the money and credit conditions in the economy in pursuit of full employment and stable prices;

· Supervising and regulating banking institutions to ensure the safety and soundness of the nation’s banking and financial system and to protect the credit rights of consumers;

· Maintaining the stability of the financial system and containing systematis risk that may arise in financial marcets;

· Providing certain financial services to the U.S. government, to the public, to financial institutions, and to foreign official institutions, including playing a major role in operating the nation’s payment system.

Organizational Structure

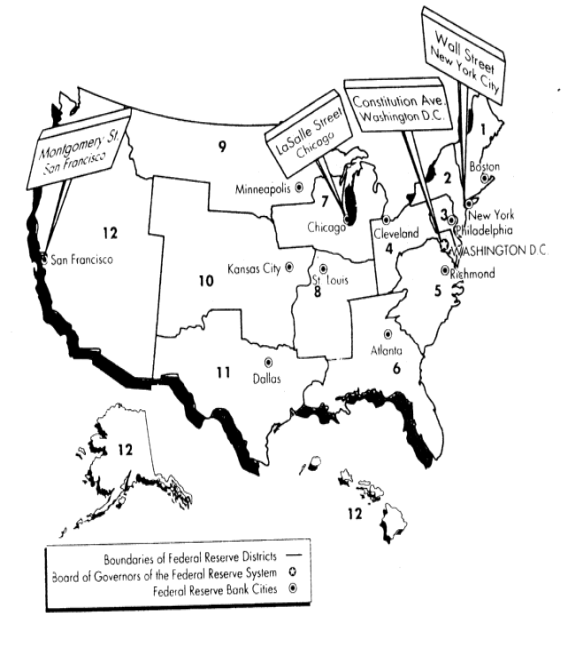

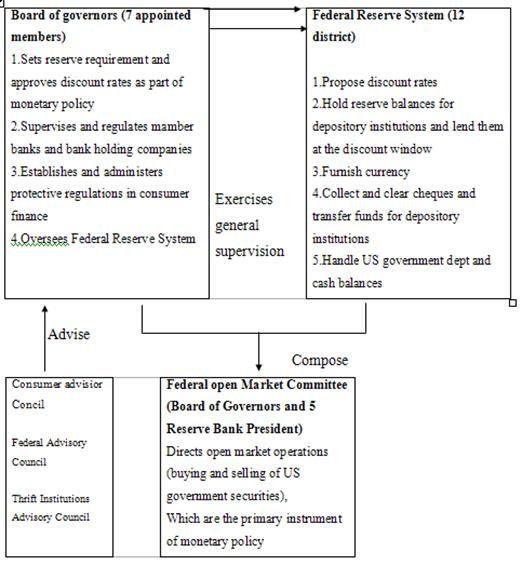

The Fed consists of 12 regional Federal Reserve Banks spread throughout the country (Figure 1) and a Board of Governors based in Washington,D.C.The Board of Governors is headed by a chairman who is appointed by the President of the United States and confirmed by the Senate for a four-year term.He or she is also one of seven members of the Board of the Governors.Board members are appointed by the President and confirmed by the Senate for 14-year term.Although unusual , a Fed chairman could remain on the board , even if not reappointed by the President as chairman , to serve out his or her regular term

The Board sets major policy for the Fed,either meeting as a Board or as the majority group on the Federal Open Market Committee (FOMC).The FOMC is composed of the seven members of the Board of Governors and five Federal Reserve Bank presidents.Each of the 12 Federal Reserve Bank has its own president , all of whom rotate on and off the FOMC.The exception is the President

Figure 1:The Federal Reserve System of the Federal Reserve Bank in New York , who is a permanent member of the FOMC.The major responsibility of the FOMC is to determine monetary policy.

Figure 2.Organization of the Federal Reserve System

Membership in the Federal Reserve System and the Dual Banking System

Commercial banks that belong to the Federal Reserve System are know as member banks.Not all commercial banks are members ,but those that are hold the majority of commercial banks deposits and assets.

Whether or not a commercial bank is member of the Fed depends on a number of factors.One important variable is whether the bank has a national or state charter to operate.Because a bank can secure a charter from a federal goverment agency or the goverment of the state in which it is headquartered , we say that a dual banking system exist in the United States.The majority of commercial banks are state chartered.Those chartered by the federal goverment are known as national banks and must be members of the Fed.State- chartered banks may or may not be members at their options.In fact , the large majority of commercial banks are not members.Since national banks tend to be larger than state-chartered banks and large state-chartered banks tend to be Federal Reserve members , however , the preponderance of bank assets and deposits are held by members banks .Large state-chartered banks that voluntarily hold membership in the Fed are usually motivated by the pestige that membership confers and their ability to take advantage of member services such as direct access to the check-clearing network.

The requirements to secure a bank charter differ somewhat at the state and federal levels, but they are all stringent , requiring among other things adequate start-up capital and background checks on its officers to ensure ethical conduct.The charte for a nationale bank is issued by the Comptroller of the Currency , a division of the United States Treasury.State charter are issued by the banking authority in the state in which the bank is to operate.National banks must have their deposits insured by the Federal Deposit Insurance Corporation (FDIC),as must state banks that are members may have their deposits insured by the FDIC , and virtually all have such insurance.

The FDIC was established in 1933 to insure commercial bank deposits and help restore confidence in a banking system heavily shaken by the Great Depression and help and the resulting financial collapse of the early 1930s.Currently commercial bank deposits are insured up to $100,000 per account by the Bank Insurance Fund (BIF) of the FDIC.A non-Federal Reserve member bank insured by the FDIC is subjects to periodic examination by the FDIC to ascertain whether it is meeting requirements,including minimum levels of capital, and following appropriate lending rules.Insured banks that are members are similarly examined by the federal Reserve System.In addition, state banks are subjects to examination by state banking officials.

The previos discussion indicates that a number of agencies can be involved in chartering, insuring, examining, and setting rules for commercial banks.Numerous proposals have been made for reducing or reorganizing the regulatory structure of commercial banking.These proposals have included vesting all examination responsibility in the FDIC because virtually all commercial banks have deposits insurance, one agency could provide uniform examinations standarts.These proposals tend to encounter considerable opposition from regulators and bankers, however, and have not been enacted.IN contrast to giving the FDIC more power, the U.S.Treasure proposed in February 1991 that many bank regulatory activities be combined in a new agency, removing much regulatory responsibility from the FDIC, thought retaining considerable regulatory responsibility for the Fed.Both the FDIC and the Fed have strongly opposed this proposal.

Bank Reserves and the Fed

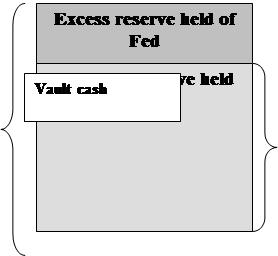

The Federal Reserve detemines the percentage of deposits that mast be held as reserves by member banks, nonmember banks, and other financial intermediaries offering checkable deposits, subject to persentage limits set by Congress.Such percentage is called a reserve requirement. To meet the requirement, reserves must be held in one of two ways.The first is vault cash-currency and coin held banks to apply to daily business needs.The second is in depository institution deposits at the Fed.These deposits account for the majority of bank reseves and require some explanation.

All member banks maintain deposit accounts at the Fed.These are noninterest-earning accounts that are similar to demand deposit accounts held by the public at commercial banks.Together, vault cash and depositary institution deposits are called legal reserves or total reserves.The portion of legal reserves necessary to meet the reserve requirement is known as required reserves, but banks may have legal reserves above the minimum.These are known as excess reservesLegal reserves are not included inany measure of the money supply since these money measures include only the amount of money incirculation.

Total (or legal) Required reserves reserves

Figure 3. Composition of bank Reserves

In addition to holding reserves in depository institytion accounts at the Fed and in vault cash, nonmember banks and other financial intermediaries may maintain their reserves on a pass-throught basis at Fed member banks (which in turn deposit these with the Fed), with the Federal Home Loan Bank System (to which most savings and loan associations belong), or a special bankers’ banks owned primarily by depository institutions to share the costs of various common financial services and do not do business with the general public.

Reserve requirement on transaction account in general exceed those on time deposits because these account turn over rapidly since they are used for transaction.Savings and time deposits are usually used for funds that are expected to be on deposit for some period of time.Technically, financial institutions can require notice to be given for withdrawal of funds from passbook savings account.In practice, however, passbook deposits are available for withdrawal at the time requested.The different function usually served by checking, savings, and time deposits have historically resulted in higher reserve requirements on checking accounts than on time and savings accounts.

3) The Federal Reserve and Monetary Policy

As the central bank in the United States, the Fed is responsible for fulfilling a number of functions,such as providing banking services to the Treasury and approving bank mergers.Another very important function and the one that attracts most attention is conducting monetary policy.This is the attempt by the Fed to unfluence the course of economic activity by affecting the reserves of the banking system.The reserve position of the banking system in turn affects the money supply, interest rates, and the economy.By making money and credit hard to obtain, or expensive, the Fed tries to reduce inflationary pressures in the economy.Alternative, by making money and credit plentiful and inexpensive,the Fed attempts to stimulate the economy.

Reserve Requirement Changes

When the Federal Reserve raises or lowers the reserve requirement, it changes the distribution between required and excess reserve in the banking system.An increase lowers the level of excess reserves, and a decrease increases excess reserves.Exess reserve availability influences the amount of bank lending in the economy.As most demand deposits come into existence throught bank lending, a change in reserve requirements may be translated into money supply changes.

Historically, the Fed has been reluctant to change reserve requirements because such action has a dramatic impact on the reserve positions of banks.Even relatively small changes absorb or release substantial amounts of excess reserve, which in turn may significantly affects the banking system’s ability to make loans. Between 1980 and 1987 the Fed was unable to use reserve requirement changes for policy purposes even if it had wanted to.The 1980 Depositary Institutions Deregulation and Monetary Control Act mandated a phase-in of new reserve requirements.Although the Fed once again has the ability to alter the requirements within rather broad limits set by Congress, it is unlikely that it will do so frequently.Nevertheless, in December 1990, as noted previosly,it did lower reserve requirements on some categories of deposits.

Discount Rate Changes

The discount rate is the rate charged banks and other depository financial intermediaries for borrowing at the Fed.Financial intermediary borrowing fulfills the Fed’s role as lender of last resort to the banking system.Since the borrowed funds go into the depository institutions’ accounts at the Fed, borrowing from the Fed leads to additional reserves in the banking system, whereas repayment of Fed loans reduced bank reserves.Presumably, borrowing would be discouraged by a rise in the discount rate and encouraged by a fall.In practice, however, the discount rate is almost always below open market rates.Therefore, financial institutions can profit by borrowing from the Fed and relending in the open market.As a results, the Fed exercises what it calls administative control over discount window borrowing to make sure that the financial institution borrowing privilege is not abused.Banks that borrow too frequently can be denied access to the discount window.From time to time the Fed has imposed a surcharge on the discount rate for too frequent borrowes.In practice, abuse of the borrowing privilege is infrequent since financial institutions are reluctant to endanger their access to the discount window.

Open Market Operations

These are the purchase and sale by the Fed of primarily U.S government securities in the money and capital markets.A purchase of securities injects reserves into the banking system, as proceeds of the purchase are deposited in bank account.Sales of securities drain reserves from the banking system as deposits at bans are used to for the securities.Thus, the banking system’s ability to lend is affected through these open marcet operations.

The FOMC, a major Federal Reserve committee, sets the General policy and issued instructions used to guide day-to-day conduct of open market operations.The Federal Reserve Bamk of Ney York,acting on FOMCinstructions,does the buying and selling of securities.In this way, the Fed is able to manage the reserve position of banks on a daily basis to meet its monetary policy objectives.

II. Depository Institutions:Commercial Banks and Banking Structure

Commercial Banking Structure

US commercial banks offer credit cards, travelers checks, travelers checks, brokerage services, and also underwrite and trade of treasury, municipal, and other permitted debt securities and can provide investment advice.

The credit philosophy adoped by American commercial banks is also somewhat different from those in other countries.Credit must be approved by a prescribed number of bank officers depending on the level of credit exposure,industry and borrewer.Accountability for decesion to extend credits are relatively easy.Credit exposure to any one one client is limited to five per cent of the total of bank capital.

Whether a bank is a national or a state bank , whether it is a Federal Reserve member or not , it must abide by the restrictions on branch banking operations imposed by the state in which it operates.In some states banks are restricted to only one office, while in other they may have several branches throughout the state.Some states fall between these extremes and permit limited branching.

Under the McFadden Act passed in 1927 , branching across state lines is prohibited to essentially all banks.The only exceptions are some very old organizations started in states before statehood and branches of foreign banks.The Bank of California , which has branches in Oregon and Washington , is the largest bank so "grandfather".However,the spread of bank holding companies , which permit banking organizations to own more than one bank or pursue banking-related business , has allowed some bank organizations to engage in branching of another kind.

Many banking services offered by banks in one state to customers in another are not strictly prohibited by the McFadden Act or are explicitly permitted by other legislation.As a results,numerous banking and bank-related services are offered nationally by a host of banks and nonbanks (financial institutions that do not technically meet the legal defiitions of banks).Although the McFadden Act has not been repealed,many analysts have concluded that its current impact is small , and United States has entered an era truly nationwide banking , therebly joing most other major industrial countries.

Internation Banking

Internation Banking refers to activities udertaken by banks outsides their home countries or directed at international business inside the bank s home country.It includes U.S. banks operating outside the United States and foreign banks operating in the U.S.Many of the large U.S. banks trace their foreign operations back more than 100 years.For example , Chase Manhattan and Citibank operated branches in Europe in the 19th

century.Recent years have seen tremendous increases in american banking overseas.

Foreign Banks in the United States

The other side of international banking is foreign bank activities in the U.S.,which increased greatly in the 1970s.

The major organizational forms of foreign banks operating in the U.S. are as follows:

Subsidiary bank:A bank that has its own state or national charter and is separate from its foreign bank owner ;it operates as a full commercial bank , accepting deposits and making loans.

Branch:A fully functioning part pf its forein bank parent.

Agency:An organization that cannot accept deposits but can make loans and provide the financing for international transactions.

Representative office:The representative office cannot accept deposits or make loans but can make contacts for its parent bank.

For many years foreign banks in the United States enjoyed advantages over domestic banks.These advantages arose mainly from the lack of branching restrictions and Federal Reserve requirements.These issued, among other, were adressed by Congress in the International Banking Act passed in late 1978, which rectified some of the inequities but did not completely eliminate them.

International Banking Act of 1978

The International Banking Act specified that foreign banks must choose a home state and restrict their growth to that state alone. However , existing operations in other states at the time the act took effects could be maintained.The provision enabled, for an example, a foreign bank with offices in NewYork and Colifornia to choose New York as the home state;it could continue to operate in but not expand in Colifornia.The choose of the home state was flexible, and banks could choose a home state where they did not have sizable operations.A bank that was already well established in New York could choose California and build a substantial operation in that state,for example.

Despite the requirement under the act to cinfine domestic bankink expansion, foreign banks can continue to expand international banking operations in other state where they are not presently located by opening subsidiaries under the rules of the Edge Act.The Edge Act of 1919, originally designed to facilitate international banking activities of domestic bank, allows any bank to open an offices are restricted to foreign lending, but Edge Act subsidiaries cannot take local deposits.

The International Banking Act also extentended FDIC insurance to deposits at foreign banks.Before the act was passed, lack of FDIC insurance showed the acquisition of retail deposits by foreign banks.The imposition of reserve requirements increased the cost of funds for foreign banks and put them on a more equal footing in lending charges with large domestic banks.By the act,the Federal Reserve, the FDIC, and the Comptroller of the Currency were granted additional regulatory powers over foreign bank operations.The Fed is now permitted to make independent examinations of any and all foreign bank operatins in the United States.

In summary, the act placed foreign banks on a more competitive footing with American banks, but it did not totally remove the advantages they enjoed, particulary in branching.However, the advent of interstate banking through state legislation discussed previously will over time remove the advantage of foreign banking operations.Although the competitive advantage may be eliminated, foreign banks will remain an important participant in U.S. banking.

1) Banking System in Transition

Prior to 1988, Ukraine's banking system was typical of centrally-planned economies. A Republic branch of the Central Bank of the USSR acted as a central bank and commercial bank for the Ukrainian industry. In the context of market-oriented economic transition, the major challenge of the Ukrainian state is therefore to establish and develop market-based banking system and financial institutions.

The banking system was. reorganized between 1988-1990. In March 1991, the Law On the Banks and Banking was adopted. It established a two-tier banking system consisting of the National Bank of Ukraine (NBU) and the system of commercial banks. The NBU is an independent legal entity, accountable only to the Supreme Council of Ukraine. The NBU consists of the Headquarters and regional branches. Its everyday operations are market-based and a centralized approach is used to regulate and distribute credits to stabilize and strengthen the national currency. The NBU implements state policy as an issuing, clearing and foreign currency center and provides services to other banks.

The National Bank of Ukraine occupies a special place in the marketization of the banking system. As a central bank of the state, it organizes and implements its own restructuring and plays a decisive part in implementing banking reforms in general. Any radical changes necessary to reform commercial banks would fail if the NBU followed a path of a command-administrative interventions in the monetary policy. The NBU has to ensure stable currency and the following:

-active interest rate policy, followed by the NBU since 1994;

-compulsory reserves of resources from commercial banks to facilitate the liquidity of the comical banks and at the same time not to allow high degree of liquidity during high levels of inflation;

-offering credits to commercial banks, using such market mechanisms as credit auctions, issuing state security bonds;

-operations with state securities in the open market, this mode was used to cover the state budget deficit in 1995.

Development of the system of commercial banks is important for the banking system|"As of 1 January 1997, 188 commercial banks with 2284 branches operate in Ukraine. During 1992-1996, 32 commercial banks were dissolved. Problems encountered by the commercial banks in the process of development were pointed out in the report to the Supreme Council of Ukraine in February 1997 by V. Yushchenko, the Governor of the NBU and were the following..

A significant and steady decline in production weakened the financial potentials of bank clients and banks themselves.

- High inflation rates also interfered with the development of

- the banking system.

- The slow pace of privatization also affected adversely the

- progress of the banking system's development.

- Imperfect or total absence of appropriate legislation, espe

- cially in the area of protecting the deposits of private individuals.

- Absence of a system of insurance for loans offered by com

- mercial banks.

- Lack of efficient personnel.

- High risk credit policy followed by certain banks to maxi

- mize profits.

- Dearth of capital of the banks.

- Untimely or default payment of loans lead to prolongation

- of the period of paying back of loans.

- Lack of liquidity leading to failure in servicing clients.

The fragile financial position of commercial banks is a direct result of their lack of rights and actual isolation from the capital markets. Unlike in other countries, restrictions imposed on commercial banks with regard to the high level of minimum statutory fund by the National Bank of Ukraine interfere with the development of financial-industrial groups and the establishment of banks as their financial instruments. This is aggravated by the fact that large volumes of-fmancial resources revolve in the informal economy in the form of cash. It is therefore important to mobilize resources into the banking system using administrative and economic tools.

Activeness of the commercial banks in providing long-term credits is low even at present when the days of unstable currency is over and Hryvnia has attained some strength. The nature of banking activity should undergo some change in order to meet investment needs and measures supporting Ukrainian banks to take part in capital markets should be encouraged.

It is high time the National Bank of Ukraine to decide what kind of banking system is optimum for Ukraine. The policy of the NBU in breaking the isolation of the commercial banks from privatization and participation in the stock markets is pertinent, however the NBU should follow a rational correlation between its general and particular policies towards commercial banks. It is necessary to avoid unified approach in identifying banks, the preferable mode being to divide them into universal and specialized ones (with certain types of functions). This opens the way for collateral, investment, savings and other types of banking activity, to which commercial banks pay less attention due to high risk, as well as facilitate the growth of state and quasi-state institutions -"development banks" which will function in the priority areas of development, agriculture, machine building etc.

Although restrictive measures are inevitable during financial stabilization, there should be a differentiated approach to statutory reserves and their terms, as is the case in FRG. In February 1996, the Supreme Council of Ukraine adopted a supplement to the law QnJdanh and^ Banking. This amendment withdrew the restrictions on banks' participation in the funds of other banks and restrictions on their activities in the securities market. The amendment revises the provision related to the bank-authorized fund that by January, 1998 must equal 1 million ECU or its license can be withdrawn. In addition, the Council prohibited the registration of foreign banks subsidiaries and increased registration requirements for banks with the participation of foreign capital (their authorized funds must be between 3 to 5 millions ECU). Finally, the Council decreed that all commercial banks would be transformed into open joint-stock companies, granting the NBU a right to formulate requirements when licensing commercial banks for specific transactions.

2) Role of the National Bank of Ukraine during transition

Before independence, when Ukraine had no national currency and banking system, the role of the central bank in such conditions consisted in implementing the financial plan and financing or refinancing loans to enterprises on the basis of this plan and provide cash in exchange of salary cheques based on payments plan. Interest rates were determined by administrative means, loans to key sectors of the economy often were made at privileged low interest rates. The banking system included central and other state specialized banks, which extended loans to various branches of the economy. At first glance, it seems to be a two-tier banking system, but in reality, this was a conglomeration of monopolists, each serving their own segments of economy. There was no place in these circumstances for monetary policy as an instrument of macroeconomic discipline, monetary policy was part of the planning process and regulated interest rate and selectively regulated credit resources. Such regulation did not aim at macroeconomic stabilization rather at achieving microeconomic ends through centralized means.

After the declaration of independence, the issue of introducing national currency as one of the attributes of an independent state was of utmost importance. Transition from the centrally planned system to a market oriented economy objectively called for exit from the ruble zone, introduction of national currency and thus creation of the bases for monetary and currency policy.Any system is characterized best by its product or result, in other words, what it gives to people in the ultimate end. The product of the banking system is - the national currency. Independent Ukraine started its journey without any monetary policy of its own, without a banking system and without knowledge of normal economic relations for 60 years. We started from a negative mark and that is why in 1992 and 1993 and part of 1994 the slogan "defending the domestic producer" was the order of the day: it was considered that the domestic producer should be helped by privileges and benefits 'and practically unlimited loans. A heavy price was paid for such a mistake - during this period inflation levels were highest in the world, and the karbovanets lost two of its most important functions: to be a unit of both value and value-added.

Radical changes in economic and monetary policy since October 1994 saved the country from national disaster. A new era emerged for the currency system in Ukraine - the currency embodied in itself that economic essence which is embedded in it by the whole history of societal development. This principle guided the activities of the National Bank during 1995-1996.

Stable currency is not only the primary condition for providing a more or less predictable level of economic management and consumption. It is a component of pragmatic systemic reform in production, in the social sphere and also in "support of effective payable demand of the population, producers and the state". A socially drientated/responsible economy starts from a stable national currency. It is impossible to set things in order in the finance sector if there is no stable currency and vice versa.

Considering this, it is difficult to discuss what should be stabilization like - "monetary-financial" or "financial-monetary". There is no sense to juxtapose measures to support balance between demand and supply ofmpney in an urgent need to introduce order in the use of resources. These are different but closely connected issues. In Ukraine, there will never be enough currency in circulation if 40% of taxes are not collected; in budget accounts everyday 1/3 or 1/2 of monthly revenues are accrued; in increasing the rolling capital of enterprises resources worth more than GDP produced is directed and in increasing the reserves of goods and assets 2/3 of GDP is spent; under conditions of constantly rising mutual indebtedness between enterprises a high degree of use value of the product is preserved in significant terms in different branches; 1/3 of profits are used for the exchequer instead of fulfilling payment obligations; under conditions of impoverishment of labor, only 14% of the. profits are used for the social sphere; while accounting mutual indebtedness, payment arrears are announced, volumes of which are 3 times less than officially recorded indebtedness. .x

The world civilization has an universal unit - stable currency lying at the basis of fair exchange of goods and services, that is, stable prices. Only stable currency paves the way to financial/ fiscal discipline and leads to economic activity.

Role of the National Bank (NBU) is important and it has been often judged as being monetarists, and is accused of disregarding priorities in order to succumb to the complexities of financial policy. Using its authority derived from law, the National Bank on rare occasions used its competence to regulate monetary-currency policy. Through the standard of national currency, the NBU ensures stable consumer prices. NBU policy during this period was aimed at achieving this goal.economic sphere and pricing based on demand and supply, has been a powerful factor of economic stabilization. The state released itself from controlling and commanding currency and immediately received a flow of currency. As a result the following tendencies were noticeable:

1.Trust on hryvnia increased. Its exchange rate became one of

2.the most reliable indicators.

3.The process of integration of Ukraine's economy with the

4.world economy was activated on the basis of liberalization of

5.economic management, where the producers and consumers exer

6.cise freedom in choosing their foreign partners.

7.Currency trade became a great economic factor for stabili

8.zation.

NBU's careful attitude towards currency trade is not an expression of monetary fetishism. The growth in volume of currency sale "extracts hot money" from the consumption market, and slows down inflation. It is also important to note, that growth of currency exchange stimulates foreign trade.

|